In his distinctively dovish Sintra speech two weeks ago Mario Draghi left the door wide open for further loosening of monetary policy in the Euro area. All options seem to be on the table to bolster European inflation numbers, including a new round of quantitative easing. Draghi’s remark about the ECB’s Asset Purchase Programme (APP) still having considerable headroom fuelled hopes amongst many market participants that net asset purchases, which ended in December last year, could soon be resumed. A revitalised APP would almost certainly comprise a new version of the Corporate Sector Purchase Programme; let’s call it CSPP2. The question is, how can credit investors position themselves in this environment?

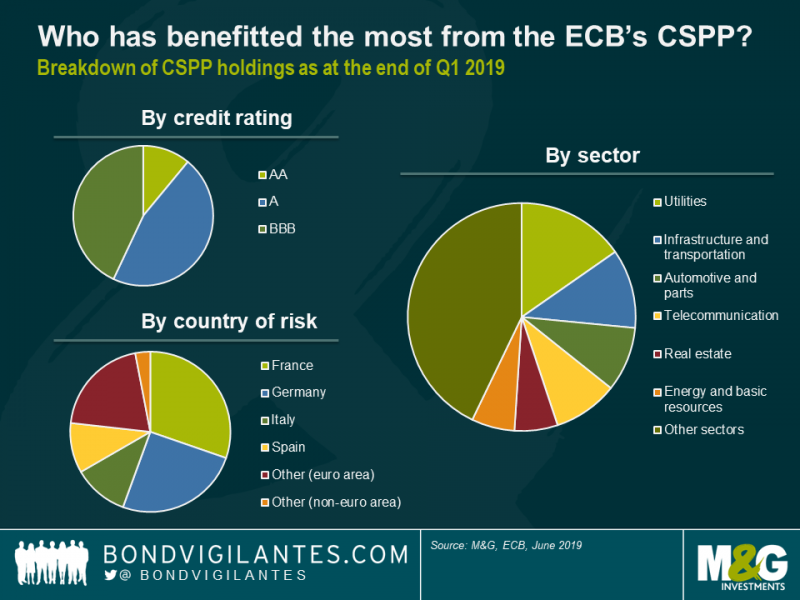

Well, it should be pointed out that current credit spread levels suggest that markets are pricing in a rather high probability of CSPP2 being announced at the ECB’s September meeting. Should the ECB fail to deliver, valuations of European corporate bonds may come under pressure. If however CSPP2 becomes a reality and is meaningful in scope, it’s fair to say that European investment grade (IG) credit by and large should benefit. Currently a sleeping giant, the ECB would once again become one of the biggest bond investors in Europe and de facto a ‘forced buyer’ of Euro IG corporates, which would pin down spread levels and quench volatility. Certain parts of the Euro IG market would of course benefit more than others, depending on where the ECB directs their purchasing efforts. If past behaviour is a reliable indicator of future asset purchases, then single-A rated bonds, French companies and the utilities sector should see the strongest technical support from CSPP2.

In his distinctively dovish Sintra speech two weeks ago Mario Draghi left the door wide open for further loosening of monetary policy in the Euro area. All options seem to be on the table to bolster European inflation numbers, including a new round of quantitative easing. Draghi’s remark about the ECB’s Asset Purchase Programme (APP) still having considerable headroom fuelled hopes amongst many market participants that net asset purchases, which ended in December last year, could soon be resumed. A revitalised APP would almost certainly comprise a new version of the Corporate Sector Purchase Programme; let’s call it CSPP2. The question is, how can credit investors position themselves in this environment?

Well, it should be pointed out that current credit spread levels suggest that markets are pricing in a rather high probability of CSPP2 being announced at the ECB’s September meeting. Should the ECB fail to deliver, valuations of European corporate bonds may come under pressure. If however CSPP2 becomes a reality and is meaningful in scope, it’s fair to say that European investment grade (IG) credit by and large should benefit. Currently a sleeping giant, the ECB would once again become one of the biggest bond investors in Europe and de facto a ‘forced buyer’ of Euro IG corporates, which would pin down spread levels and quench volatility. Certain parts of the Euro IG market would of course benefit more than others, depending on where the ECB directs their purchasing efforts. If past behaviour is a reliable indicator of future asset purchases, then single-A rated bonds, French companies and the utilities sector should see the strongest technical support from CSPP2.

However, trying to ‘front-run’ the ECB—or any other central bank for that matter—is a tricky business. The particulars of CSPP2, if it ever sees the light of day, are still unclear. The ECB may well surprise markets again, just like in March 2016 when the ECB outlined the original CSPP and most market participants had not anticipated that weak BBB-rated credit and even cross-over names would be CSPP eligible. The big twist this time round could be the inclusion of senior bank bonds, which the ECB hasn’t been buying in the past. Adding bank bonds to the CSPP2 shopping list would greatly expand the ECB’s investible universe; banks account for nearly 30% of the broader Euro IG universe. Supporting credit spreads of bank bonds, and thus lowering the funding costs for European banks, would also help soften the blow to banks’ profitability of further interest rate cuts that might be announced alongside CSPP2. The inclusion of bank bonds would not be without problems, though. Conflicts of interest could arise for the ECB which would effectively help fund the very same institutions it is supposed to regulate and supervise.

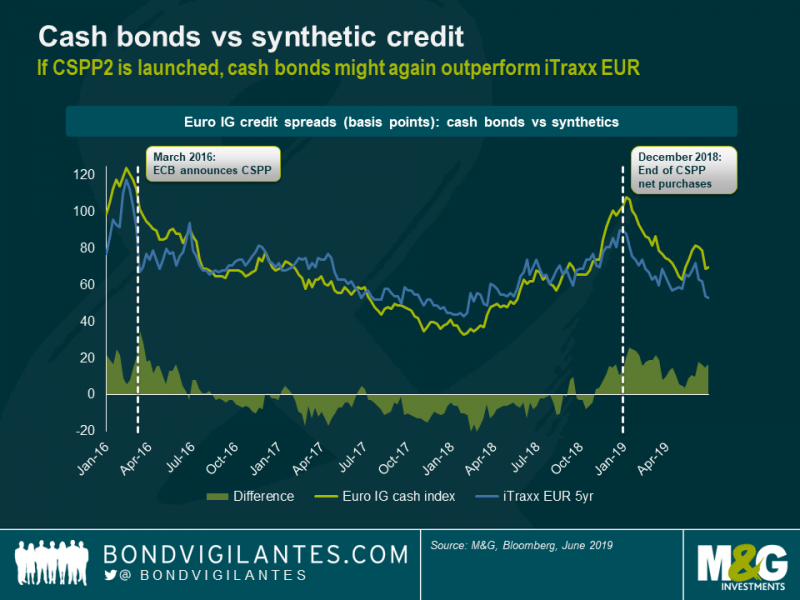

Irrespective of the finer details, the launch of CSPP2 would also have a profound impact on the so-called credit default swap (CDS) basis, i.e. the relationship between the credit spread levels at which CDS contracts (synthetic credit) and corresponding corporate bonds (physical credit) are trading. Under CSPP2, the ECB would directly interfere in the physical credit market by purchasing large quantities of Euro IG cash bonds. All else being equal, the increased demand for corporate bonds would push their credit spreads lower. The strength of physical credit would likely feed through to synthetics, but considering that the ECB wouldn’t directly intervene in the CDS market, chances are that physical bonds would outperform synthetic credit.

That’s exactly what happened last time. Before the ECB announced the original CSPP in March 2016, the broad Euro IG cash bond market was trading wider than iTraxx EUR, the benchmark European IG CDS index. Over the course of the following two years, when the CSPP was in full swing, physicals outperformed synthetics considerably. Only when the ECB started to gradually scale back net purchase volumes in 2018 (and liquidity considerations became relevant in the Q4 market sell-off) did cash bonds widen again beyond the CDS market.

At the moment, investors are paid around 20 bps more in credit spread for owning the physical Euro IG market vs selling protection on iTraxx EUR, which is a meaningful differential considering prevailing spread and yield levels. I don’t think the current relationship makes a lot of sense, to be honest. If the market fundamentally believes that CSPP2 is around the corner – and the recent credit rally certainly doesn’t suggest otherwise – then shouldn’t investors want to buy physical bonds rather than writing CDS, considering the likely outperformance of the former over the latter? In my view, this makes cash bonds look relatively cheap compared to synthetics. Investors can currently buy corporate bonds and (partially) hedge credit beta via CDS (i.e., offset credit market risk by buying protection on iTraxx EUR), thus creating a position that offers both a positive spread carry and upside if CSPP2 is eventually launched.

Dr. Wolfgang Bauer, Fund Manager Fixed Income, M&G Investments

07/08/2019

Swiss Fund & Finance Platform