Ethna-DEFENSIV

- Fund delivers good performance for the month despite climbing interest rates in the U.S.

- Fiscal support programmes on both sides of the Atlantic remain a cause for concern

- Falling inflation and weaker economy in the Eurozone slow the rise in yields

- Peak interest rates in sight both in the U.S. and Europe: better risk/reward ratio for higher duration

31 October 2023 – In October, bond investors saw a spectacular rise at the long end of the U.S. yield curve. 10-year U.S. Treasury yields briefly topped the 5% mark: their highest since 2007. Two main factors were at play here: U.S. consumer spending was surprisingly strong, as seen in the robust figures for the retail trade and GDP growth of 4.9% in the third quarter (annualised); and market participants remain concerned about very generous fiscal supports both in the U.S. and Europe. The U.S. budget deficit rose from 1.4 trillion (5.4% of GDP) in fiscal 2022 to 1.7 trillion (6.3% of GDP) in fiscal year 2023. On this side of the Atlantic, the Italian government published its budget for 2024, which confirmed the expected deterioration in budget revenue compared with the figures released in the spring. Large-scale government programmes are unsettling bond investors over the ability/willingness of the respective governments to bear the cost of interest. In the U.S., this was clear from the lower demand in the latest auctions for longer-dated U.S. Treasury bonds.

In Europe, however, increases in yields were held in check by the generally weak macroeconomy: on 31 October came the announcement that EU economic output shrank in the third quarter of 2023. Moreover, the survey-based business climate indices remain low, which suggests further relative weakness in the EU. Our almost exclusive positioning in euro-denominated sovereign and corporate bonds delivered very good results in October: over the month, the Ethna-DEFENSIV gained 70 basis points despite the losses in bond and equity markets.

An additional driver behind the relative outperformance of European bonds over their U.S. counterparts was the inflation dynamic in both economies. European headline inflation (HICP) fell below the 3% mark in October, at 2.9%, compared with 4.3% in September. Core inflation fell from 4.5% in September to 4.2%, as the prices of both services and goods came down. In the U.S., on the other hand, inflation was largely unchanged from the previous month, at 3.7%, with gasoline prices being the component that rose the most. U.S. core inflation fell slightly but remained above the 4% mark.

Our portfolio duration is currently 3.8. This relatively low interest-rate sensitivity sets us apart from most of our competitors and led to an outperformance in October because European yields fell, in particular in the 3 to 7 year range. In the context of our macroeconomic outlook (i.e. the probability of further interest rate rises is low), the question for us is whether the most attractive time to increase our portfolio duration is now or in the near future. For some time now we have been considering expanding our futures positions in 10-year German or U.S. sovereign bonds. To date, we have only opened a small position of approx. 5% in bond futures. The spread between the 10-year U.S. and German sovereign yields recently topped the 2 percentage point mark, which makes U.S. Treasuries more attractive. At the same time, we are wary of the upward dynamic at the long end of the U.S. yield curve, and remain cautious for the time being. Should U.S. Treasury yields climb further, we will seize the opportunity and increase our duration by taking out futures on long-dated U.S. Treasuries.

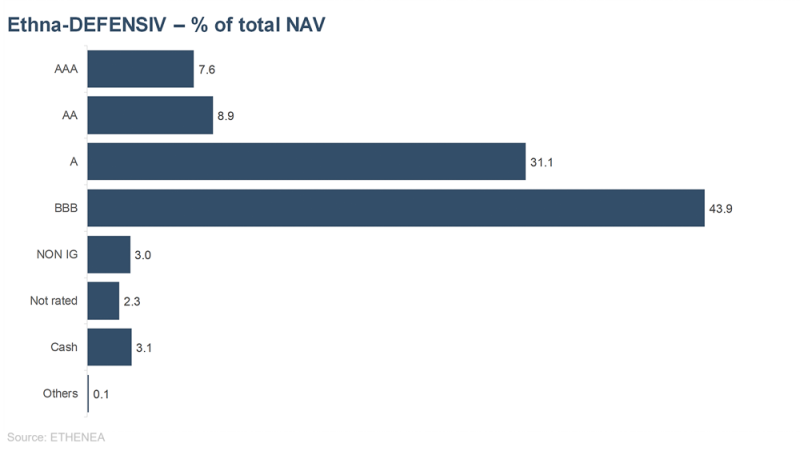

Figure 1: Portfolio structure* of the Ethna-DEFENSIV

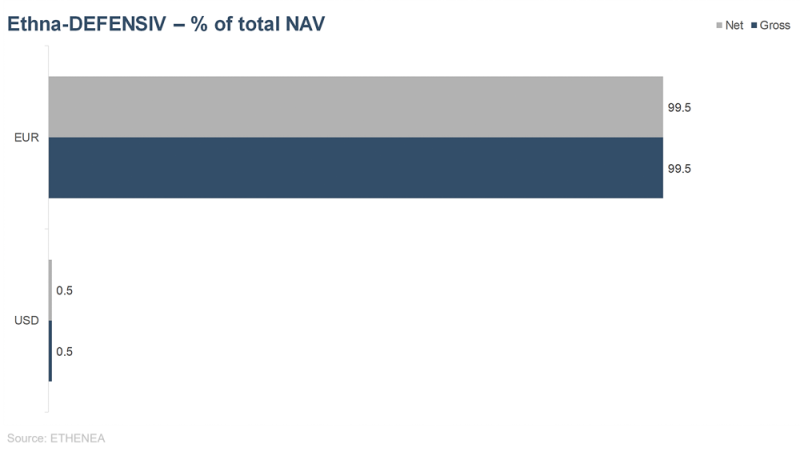

Figure 2: Portfolio composition of the Ethna-DEFENSIV by currency

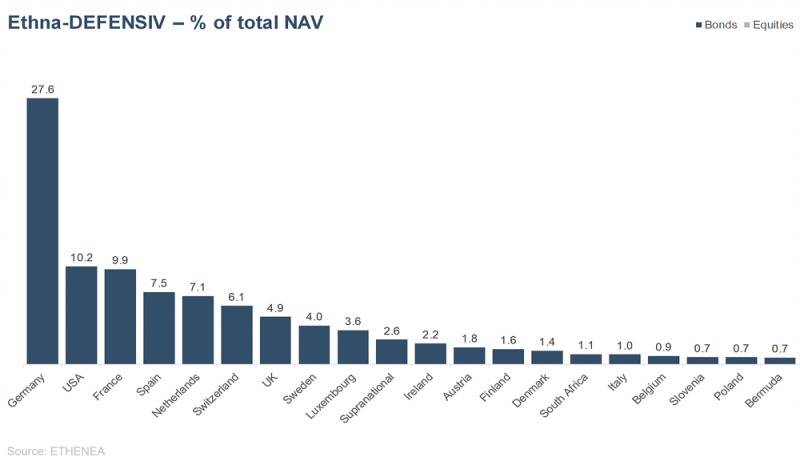

Figure 3: Portfolio composition of the Ethna-DEFENSIV by country

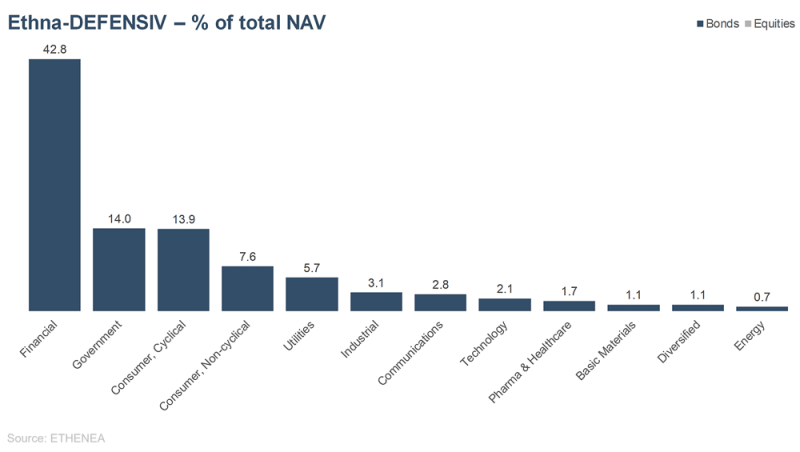

Figure 4: Portfolio composition of the Ethna-DEFENSIV by issuer sector

Author: Dr. Volker Schmidt, Senior Portfolio Manager

Ethna-AKTIV

- While European interest rates trended sideways, U.S. interest rates continued to rise, putting pressure on risk markets.

- Modified duration was further increased from 4.4 to 5.0.

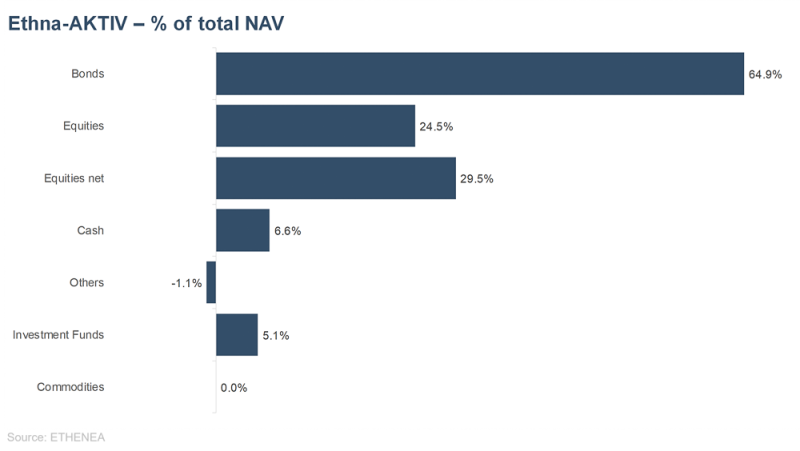

- Equity allocation was adjusted by a further 5% to manage risk. The current net equity allocation is 29.4

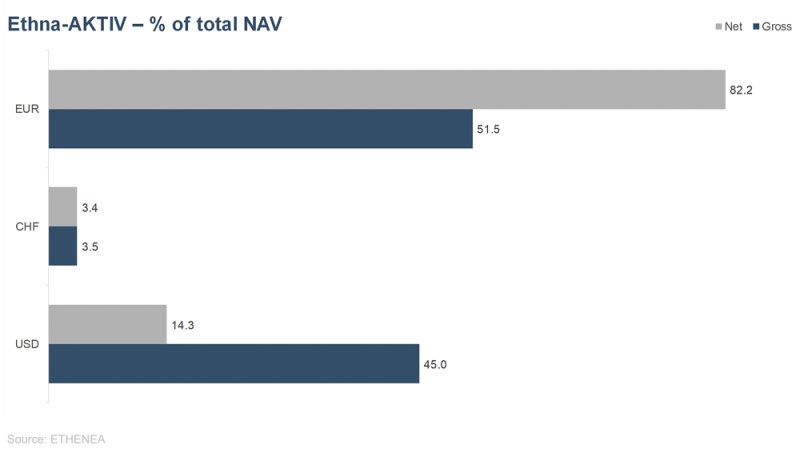

- Foreign currency exposure to the U.S. dollar was increased to 14.3% and exposure to the CHF was kept constant, at 3.4%.

31 October 2023 – The Ethna-AKTIV fell in October in lockstep with global markets. While European interest rates barely moved at the long end, the ongoing upward pressure on U.S. interest rates created a stiff headwind in risk markets. Nor did the unexpected terrorist attack on Israel and the subsequent renewed escalation of the Middle East conflict help matters, even though the market reaction has so far been contained. What is remarkable in this context is the very slight-to-non-existent reaction of the U.S. dollar and U.S. Treasuries, which, currently, are apparently not or not yet acting as a safe-haven investment. Only the price of gold again topped the USD 2,000 mark due to the geopolitical situation and despite rising real interest rates. Against this backdrop, not even a strong earnings season could translate into a positive price dynamic. On the contrary – the prices of even the technology heavyweights that have been shoring up the index to date increased rather insignificantly or even fell in response to the fundamentally good earnings figures. While this amounts to a correction of around 10% in the broad S&P500 since the summer, prices of second-tier stocks (Russell 2000 or MDAX) have already slid by almost 20%, a fall in or around the lows of last year. Not much new happened on the central bank front. Despite pausing hikes, the “higher for longer” mantra is being repeated ad nauseum. The ECB left its key rate unchanged, and we expect the Fed to do the same. Of course, we must also bear in mind here that the rising yields in the capital market themselves are creating a more restrictive environment, and have thus done some of the work for the central banks.

Since we still do not share the macroeconomic pessimism of many doomsayers and still expect moderate growth with no U.S. recession in the next few months, we have only made minor changes to the portfolio. Equity exposure was reduced by a further 35% to just below 30%, and portfolio modified duration was increased only slightly to 5.0. We are still working under the assumption that interest rates have peaked or are close to peaking. However, to enable us to increase duration markedly as planned, we want to be sure that interest rates have definitively turned the corner. We think it unwise to take up a positioning too soon contrary to such a strong momentum. A little more patience is required in this respect. We made a more significant adjustment with regard to the U.S. dollar allocation, raising it from 9.5% to 17.5%.

In summary, consistent with our investment philosophy, the portfolio structure is robust and conservative to both withstand further volatility and participate with attractive results in a potential year-end rally, which is something we also continue to expect.

Figure 5: Portfolio structure* of the Ethna-AKTIV

Figure 6: Portfolio composition of the Ethna-AKTIV by currency

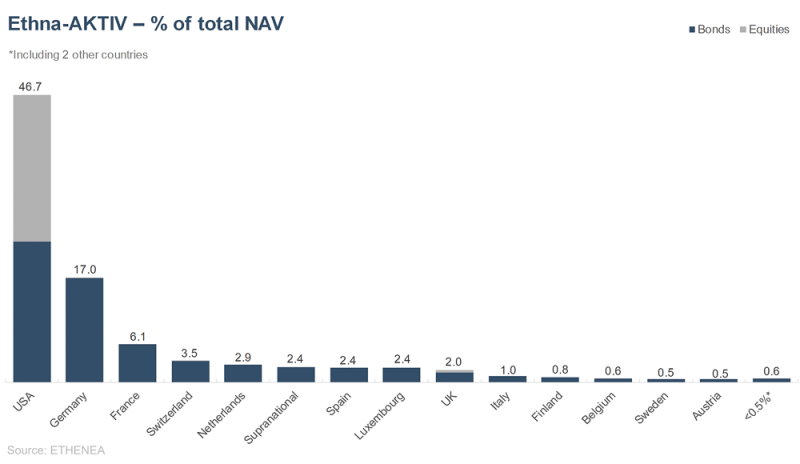

Figure 7: Portfolio composition of the Ethna-AKTIV by country

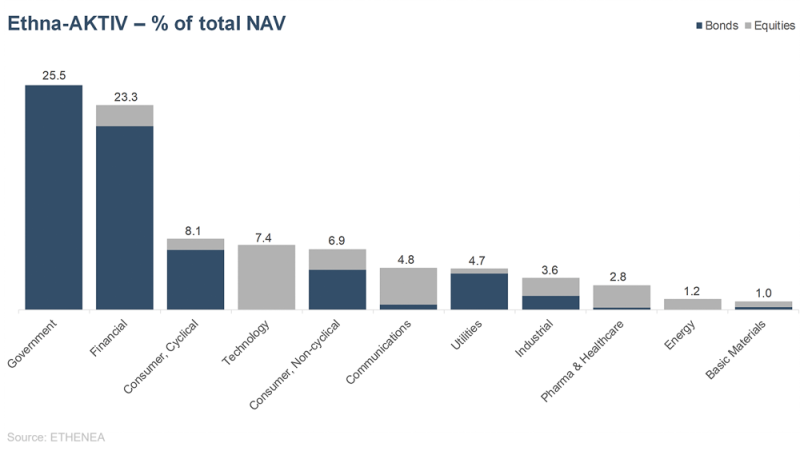

Figure 8: Portfolio composition of the Ethna-AKTIV by issuer sector

Author: Michael Blümke, CFA, CAIA, Senior Portfolio Manager

Ethna-DYNAMISCH

- Bond and equity prices recorded further falls in October.

- The risk/reward profile of equities holds potential, which we take account of with a substantial equity allocation of 67%.

- Long-dated U.S. Treasuries were given an allocation again for the first time in more than two years.

31 October 2023 – In October, the previous month’s capital market trends continued. Rising yields in bond markets caused prices to fall in equity markets. In many cases, new record price lows for the current cycle were seen. In particular, second- and third-tier smaller-cap equities again came under strong selling pressure. Lower-risk alternative investments such as time deposits, money market funds and short-dated sovereign bonds have gone up in popularity with many investors in step with higher interest rates, while demand for higher-risk investments such as equities, corporate bonds and longer-dated bonds has fallen considerably. Overall, the risk/reward ratio of these investments should gradually improve as prices comes down, as we outlined and also implemented in the portfolio back in September. We wrote in last month’s Market Commentary:

“Together (these factors) led us to increase the net equity allocation at month-end to around 67% (as a result of the complete reversal of our hedging). This is a reflection of the slightly improved risk/reward profile. But we are not venturing too far out in the open, as the danger has not gone away. Overall, our assessment of the market tends to be balanced.”

Nothing has happened to change this assessment. Not breaking cover was obviously necessary and could remain so in the short term, as even though company fundamentals are proving amazingly robust this earnings season, the effects on share prices has been less positive overall. Investors’ extreme nervousness was palpable at all times and companies got punished on the stock market for disappointing on expectations even slightly. Until then, however, the stocks held in the Ethna-DYNAMISCH were largely satisfactory – both in terms of fundamentals and the direct effects on share prices. The fund’s latest fall in price was first and foremost a reflection of the general weakness in equity markets. This weakness arose, on the one hand, out of the ongoing pressure on relative and absolute equity valuations due to the further increase in bond yields, as mentioned above, and, on the other hand, out of the high level of uncertainty about further economic growth. On that note, we refer once again to September’s Market Commentary, where we wrote:

“In addition, we are keeping a close eye on developments in the bond market. Long-dated U.S. Treasuries, whose yields soared in September, constitute an increasingly attractive option to hedge the portfolio against economic risks.

In October, we seized this opportunity and, for the first time since July 2021, we built up a position in long-dated U.S. Treasuries once more. Up until summer 2021, these bonds time and again contributed a great deal to the portfolio before the rise in inflation and yields became the dominant theme of the past two years, and the prices of long-dated sovereign bonds tanked. This historic process of adjustment in interest rates and yields is, in our opinion, well advanced, with the result that sovereign bonds with the highest credit ratings again constitute an increasingly attractive component of asset-management portfolios.

A brief note on the backdrop: in periods of increasing stress in the capital markets and, in particular, when recessionary risks are mounting, investors are drawn to the safest and most liquid investments, which include, in particular, U.S. Treasuries. As demand increases, prices rise (which pushes down yields) and, as a rule, market-wide expectations for central banks to cut interest rates also increase very quickly. What is interesting about long-dated U.S. Treasuries – we focus mostly on the 30-year segment – is that prices react disproportionately more to changes in yield. The U.S. Treasuries that we purchased in October with an initial allocation of around 5% of the fund were issued in 2020 with 30-year maturities, yields of less than 2% and prices of 100. Today the yield is around 5%, giving purchase prices of less than 50. The modified duration, which indicates how sensitive the bond price is to a change in yield, is around 20 for these bonds. In other words, if yields fall from 5% to 4%, these prices of these bonds would go up by roughly 20%. However, since the opposite also applies if the yield rises from 5% to 6%, we are being very cautious at the moment and intend to expand the position to approximately 10% to 15% of the fund – similar to past volumes – either over time or countercyclically, at times when yields are rising further.

In summary, the latest falls in prices in bond and equity markets have made the scenario for medium-term performance expectations more and more attractive. The net equity allocation of the Ethna-DYNAMISCH is currently at its highest year to date and we are thus poised to take advantage of these opportunities. At the same time, given the bond market situation outlined above, the active portfolio management toolkit has broadened greatly, with the result that a key component of risk management can again be meaningfully employed going forward.

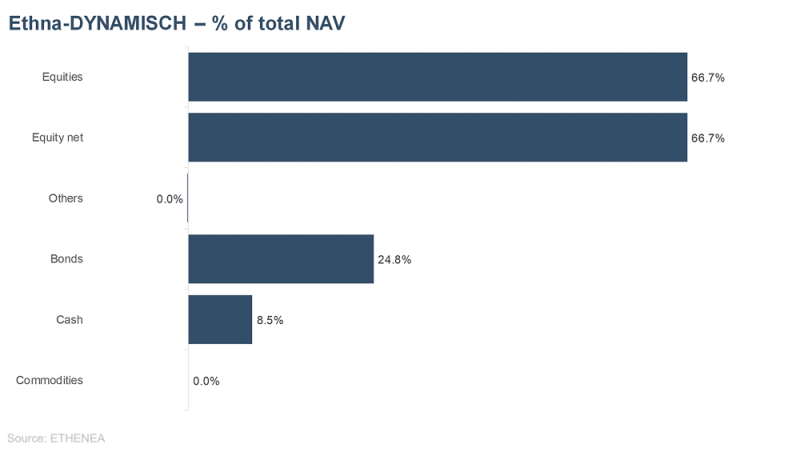

Figure 9: Portfolio structure* of the Ethna-DYNAMISCH

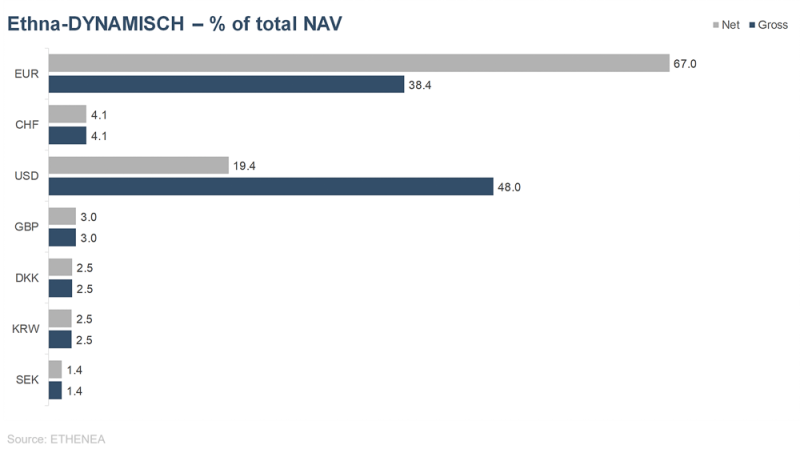

Figure 10: Portfolio composition of the Ethna-DYNAMISCH by currency

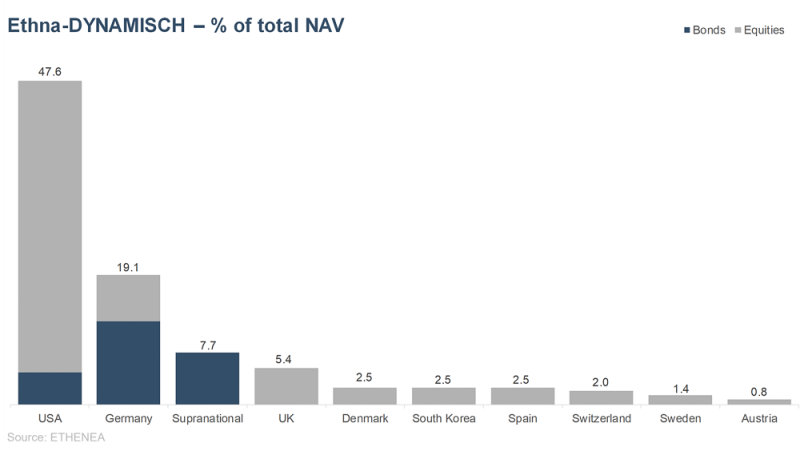

Figure 11: Portfolio composition of the Ethna-DYNAMISCH by country

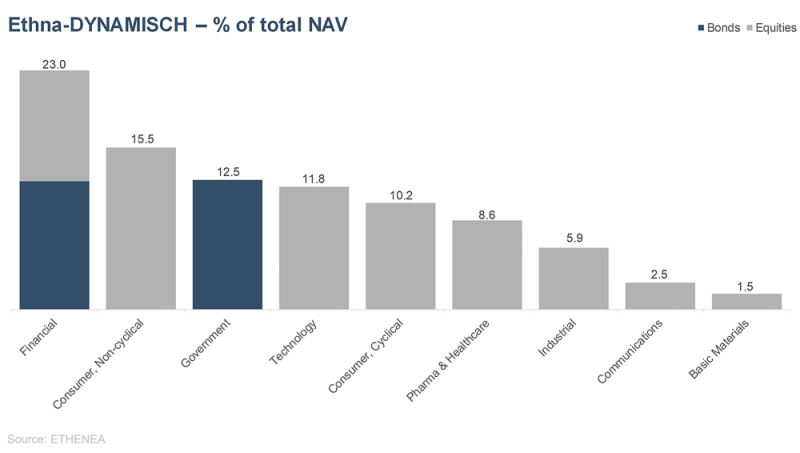

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Author: Christian Schmitt, CFA, Senior Portfolio Manager

HESPER FUND – Global Solutions (*)

- In October, global yields continued to rise

- Fears of war escalation sparked an initial strong rally in oil prices

- US consumer prices rose at a brisk pace for the second month in a row

- Global equities tumbled as yields soared

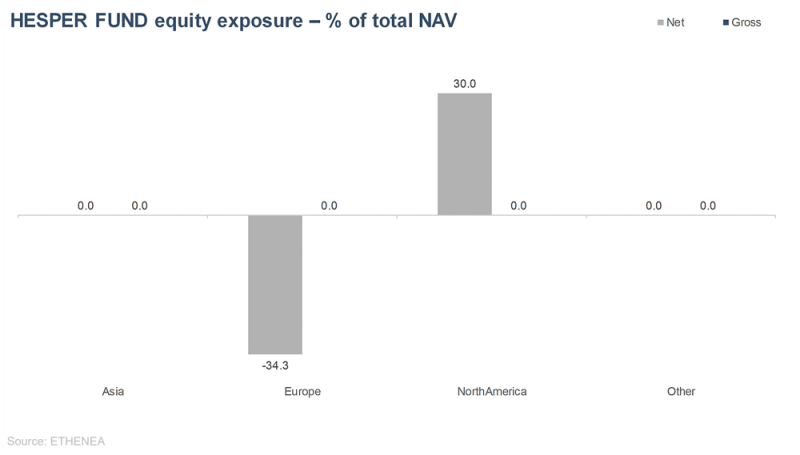

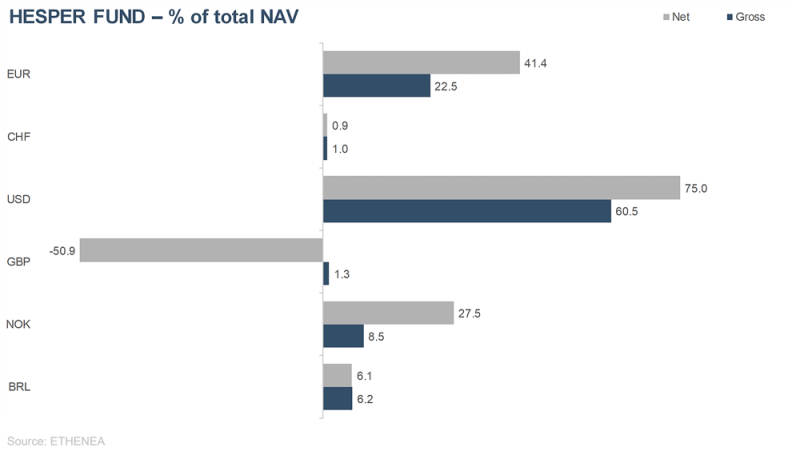

- The HESPER FUND – Global Solutions rebalanced the portfolio to reflect the change in sentiment and re-pricing of the rate trajectory. Duration was kept in negative territory at -1.8 years. Overall, net equity exposure was reduced from neutral to slightly negative, being long US equity indices and short European indices such as UK mid-caps, European banks and the DAX. In FX, the fund adjusted non-performing bets, reducing the Norwegian krone exposure to 27% and cutting the GBP short to -50%. Dollar exposure was increased to 74%.

31.10.23 - Hot US economic data fuelled Fed bets and pushed bond yields to multi-year highs

Despite the outbreak of war between Israel and Hamas, government bonds have not been the place to hide. The surprising strength of the US economy and a ballooning federal deficit are challenging the Fed’s attempts to tame inflation. On the other hand, higher Treasury yields are helping to tighten financial conditions and may restrain the Fed from tightening further. In September, US inflation ticked up for the second month in a row. As a result, the US yield curve continued to steepen (less inverted). The US economy has further defied pessimistic forecasts and the Treasury has flooded the market with new bond issues at a time when traditional buyers, including the Fed and other major central banks, are pulling back.

While Powell signalled that the Fed may stand its ground at the upcoming FOMC meeting, solid economic data and higher inflation expectations are keeping the Fed on alert.

Global stocks slumped as yields rose

Yields became the main driver of equity markets. The bond rout dragged down equities almost everywhere. Fears of an escalation of the war in the Middle East and oil volatility added to market uncertainty.

The equity sell-off continued in October as global markets slumped for the third consecutive month amid higher yields. Decent quarterly earnings growth in the US was not enough to support the markets. The DJIA and the S&P 500 lost 1.4% and 2.2% respectively. The tech-heavy NASDAQ plunged 2.8% and the Russel 2000 tanked 6.9%.

In Europe, the Euro Stoxx Index was down 2.7% (-2.7% in USD) while the FTSE 100 fell 3.8% (-4.2% in USD). The Swiss Market Index declined 5.2% (-4.7% in USD as the Swiss franc strengthened).

In Asia, Chinese equities were unable to halt their slide, as property woes continued despite the government’s many efforts to stimulate markets and the economy. The Hang Seng plunged 3.9% (-3.8% in USD) and the CSI 300 dove 3.2% (-3.4% in USD). Japan’s Nikkei lost 3.1% (-4.8% in USD) as the BoJ adopted a more flexible approach to yield control. The Korean stock market tumbled 7.6% (-7.2% in USD).

Macro scenario of the HESPER FUND - Global Solutions: too early to cut

The global economy remains resilient to much higher nominal interest rates, as fiscal support, labour market strength and accumulated savings continue to support consumption. Surveys of future activity are again gloomy, but the hard data remains relatively weak, with few signs of an imminent recession.

Our medium-term macroeconomic outlook is for a further slowdown in the global economy over the coming quarters. Thanks to a surprisingly solid US economy and the increasing efforts by Chinese authorities to stimulate growth and address the problems in the property market, the global economy will avoid a recession any time soon. However, the Eurozone economy is already losing momentum and faces a few quarters of stagnation or moderate contraction. Given the long and variable effects of monetary policy, it is too early to exclude the possibility of a recession in 2024.

Inflationary pressures will gradually abate as core prices remain sticky. However, the recent volatility in oil prices threatens the smooth disinflationary process and, if it persists, could trigger a second wave of inflation.

The contraction in monetary growth is now in place and will eventually dampen demand, but, with fiscal stimulus in advanced economies still strong, central banks will not be in a position to loosen policy any time soon. The Fed’s message of “higher for longer” has been clearly heard by the markets, which have adjusted accordingly. In addition, the war in the Middle East continues to cloud the economic outlook. Iran’s involvement could derail all forecasts and lead to even greater market volatility. We are keeping our fingers crossed as the West steps up its efforts to prevent a wider conflict.

Central banks that have already adopted a data-dependent stance may be at or close to the peak of the interest rate cycle. However, it is far too early to think about a policy reversal. Interest rates will remain higher for longer in order to bring inflation down to the 2% target, and we do not expect any cuts in the coming quarters. If the decline in inflation is delayed, or if inflation reaccelerates, central banks will have to tighten policy further, which will increase the risk of recession.

Positioning and monthly performance

The HESPER FUND – Global Solutions decreased in October (unit class T-6 EUR -1%) as NOK exposure and L/S duration strategies weighted on performance.

The fund reduced its overall equity exposure to 0% or slightly negative at certain moments, being long on US equities and short on some European indices. The fund maintained a negative duration exposure at 1.8 years, as we believe that interest rates and yields will have to rise further to contain inflation. The fund continued to trade actively in FX, increasing the dollar exposure to 74%.

The MTD (-1.46%) attribution was -0.22% fixed income, +0.41% equities, +0% commodities, -1.54% currencies and -0.11% fees and expenses. The weakening of the Norwegian krone and a slight decline in the dollar weighed on results. Decorrelation with traditional assets such as equities and bonds remained high.

Year–to-date the fund is at -4.94%. Total assets decreased to EUR 65.3 million at the end of the month. The unit is 11.3% below its all-time high on 29 September 2022.

Volatility over the last 250 days ticked down to 4.5%, maintaining an attractive risk/return profile. The annualised return since inception decreased to 2.8%.

As we enter November, the fund continues to stay far away from its reference currency and to trade actively in FX. The euro exposure is now only 40%. Currently, the currency exposure is as follows: USD 74%, NOK 27%, CHF 0.9%, BRL 6% and GBP -50%.

As always, we will continue to monitor and adjust the fund’s exposure to the various asset classes in line with market sentiment and changes in the macroeconomic baseline scenario.

Figure 13: Equity exposure by region of the HESPER FUND − Global Solutions

Figure 14: Currency allocation of the HESPER FUND − Global Solutions

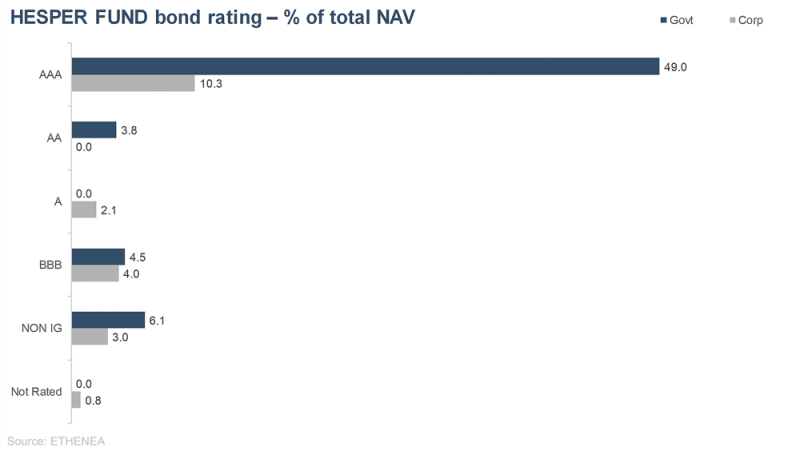

Figure 15: Bond rating structure of the HESPER FUND − Global Solutions

*HESPER FUND - Global Solutions is currently only authorised for distribution in Germany, Luxembourg, Belgium, Italy, France, Austria and Switzerland.

Author: Federico Frischknecht, Senior Portfolio Manager