Cloud computing allows companies to access virtually limitless computing power and storage on a pay-as-you-go basis. Any organisation – from a start-up to a government – can have access to world-class computing resources cheaply and quickly. The computing infrastructure itself is owned and operated by the ‘hyperscale’ cloud companies Amazon (AWS), Microsoft (Azure) and Google (GCP). When individuals stream videos, play games, use social networks and bank online they are often using physical computing resources sitting in the cloud. Pinterest, Instagram and Facebook are all example of an applications that uses cloud computing to store photographs and apply machine learning or artificial intelligence to identify the images and present consumers with more relevant content to their interests (including targeted advertising). More importantly it also allows businesses to save the cost of having to own, maintain and manage their own data centres (servers, storage and networking) while still having the ability to provide full computing capabilities. Cloud computing is a key part of businesses’ digital transformations as they modernise not just to evolve but to survive.

Most enterprise software is now also delivered in a rental model known as Software as a Service (SaaS) which is delivered via the cloud in a multi-tenant environment (multiple clients per server), significantly improving hardware utilisation and democratising access to technologies previously accessible to only the largest enterprise companies.

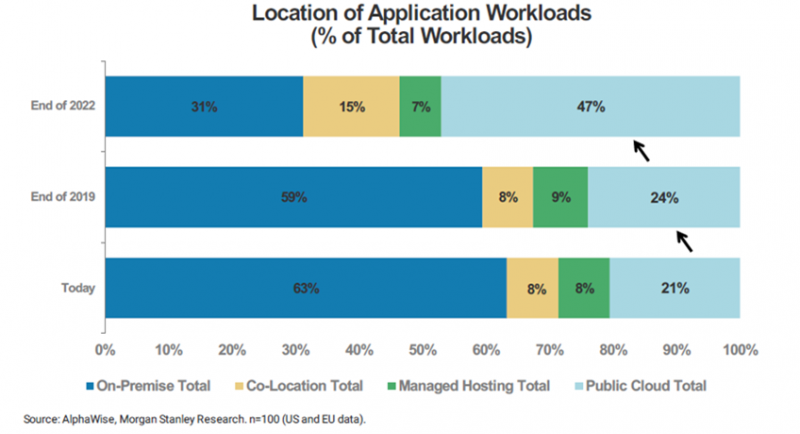

Where are we now?

The cloud computing industry is dominated by three big players. Amazon Web Services (AWS) is Amazon’s cloud platform that was launched in 2006 and is the market leader. To give an idea of the scale of the business, in Q3 2019 alone it generated $9bn in revenues, up 35% on the previous year, with a profit margin of 25%. Azure, launched in 2010, is Microsoft’s equivalent that recorded $4.2bn in revenue over the same timeframe (up 59% y/y). Google’s GCP (Google Cloud Platform which forms Google’s ‘other revenues’ includes G Suite/Google Play) produced $6.4bn (up 39% y/y).

Three main categories of cloud computing service have developed: Infrastructure as a Service (IaaS), the significantly larger SaaS and the intermediate Platform as a Service (PaaS), where the consumer provides the software and the provider provides the network, server and operating system.

Survival of the biggest and brightest

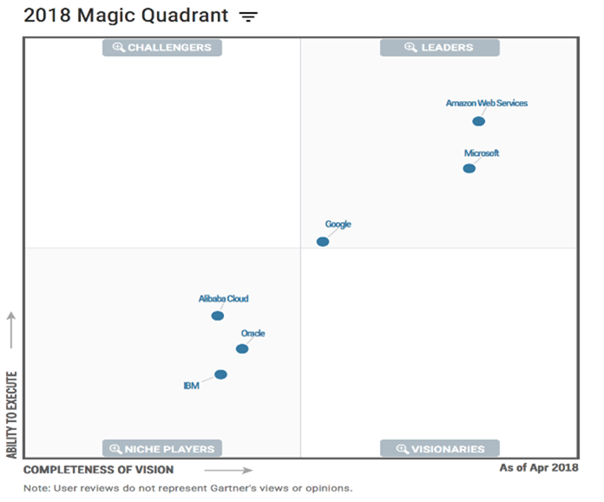

IaaS is essentially the storage and network building blocks of any cloud service and is rapidly forming around a handful of companies. A year ago, research firm Gartner produced an IaaS ‘magic quadrant’ of 15 leading cloud companies; this year there are just six. Gone are the telcos and managed service providers leaving three vendors who – thanks to their massive scale – deliver high levels of performance, fault tolerance and availability.

Where next?

As cloud offerings continue to broaden and deepen so more uses are found for the cloud and the total addressable market expands again. This leaves a lot of room for conjecture. For example, Gartner sees the opportunity at more than $1trn while KeyBanc believes nearer $1.8trn is up for grabs. Fortunately, either scenario should provide plenty of runway to sustain cloud growth well into the next decade.

Like electricity before it, the cloud has become both the source of and saviour from disruption, with cloud computing now providing the infrastructure to help businesses drive their digital transformation.

The next decade will be about Artificial Intelligence…

The past 18-24 months has seen the commercial application of AI and machine learning (ML) take off as companies across a myriad of industries embraced AI-infused automation and incorporated them into daily workflows in order to streamline operations in a new world informed by data.

It is important to differentiate here. True AI is where decision-making is based on self-enhancing algorithms – this is the very definition of AI. All too often, companies we see are claiming to use AI when in fact they are using automated rules-based decision engines where the rules are written and enhanced by humans. There is also a lot of hype around AI superiority, artificial general intelligence and the singularity (ie when technology is so superior/masterly it takes over from humans for good – fortunately this is a worry for decades into the future).

In the meantime, and much more relevant to investors, is the very significant recent progress in narrow AI where machines are used to solve specific tasks and thereby work with or enhance human capabilities. The only issue is that sophisticated deep-learning models do not offer the traceability to establish which factors have played key roles in the prediction/decision-making. This means that an AI algorithm, trained and improved with specific data sets, cannot immediately be transferred to process another distinct data set with a similar success rate, however lessons learnt can be transferred into other areas igniting innovation.

There have been some very significant AI developments in 2019:

Through the first nine months of 2019, $13.5bn in venture capital has been raised by 965 AI-related companies in the US. This compares to $16.8bn raised in the full year 2018. The 2018 investments represented an increase of more than 35x on the amount invested in 2010, while ML and computer-vision platforms have attracted the largest cumulative investments after ML applications.

In July 2019, Pluribus, a poker-playing AI engine designed by a Carnegie Mellon and Facebook AI team, beat 12 professional Texas Hold’em poker players over a 12-day session consisting of more than 10,000 hands. Most AI engines work forwards through decision trees to determine the best move. In this instance, Plurius taught itself from scratch and improved by looking back at what it could have done better. By playing millions of hands of poker against copies of itself, it created a blueprint and then looked a few moves ahead to predict how a particular decision may play out. It is this ‘limited look ahead’ algorithm that was the major breakthrough relative to the computationally-intensive task of looking ahead to the end of the game. As a result, it computed its blueprint strategy in just eight days using a 64-core server and used just 28 cores (2x Intel Haswell 14 core CPUs) during live play (versus 1920 CPU and 280 GPUs used by DeepMind’s Alpha Go victory against Lee Sedol in 2016) and plays a hand in 20 seconds, twice as fast as professional humans.

In October 2019, Google-owned DeepMind’s StarCraft 2 AI also made a significant breakthrough, reaching grandmaster level playing the real-time strategy game (beating 99.8% of humans). DeepMind’s AI uses artificial neural networks to recognise patterns from large data sets and learn from first watching videos of professionals, then from simulated game play against itself. It took 44 days of playing (the equivalent of 200 human years of playing Starcraft) to reach grandmaster status, using 384 specialised tensor processing units (TPUs) created by Google specifically for AI. Once trained, it also was able to run on a regular gaming laptop.

What does this mean? How are these relevant?

The goal with these advances is to develop AI algorithms so they can better human performance in virtually any competitive, cognitive challenge and in combination these recent advances highlight the incredible pace of innovation. By attempting to solve complex multi-player games like Poker and Starcraft, the foundations are being laid for significant advances in AI which can be applied to many areas including self-driving cars, healthcare, security and many other kinds of simulation.

For now, a disproportionate amount of incremental investment in commercial AI has been directed towards natural language processing and computing vision applications, driven by strong commercial demand for robotic process automation (RPA), AI-assisted diagnostics, and intelligent customer service and so on, mostly within the technology sector.

While some are suggesting the pace of innovation in our sector is slowing, we believe the opposite. Cloud computing has democratised IT. Combining cheap, easily accessible computing and storage with advances in AI is incredibly powerful force. The technology sector is seeing this influence now across areas such as e-commerce, advertising, digital media/TV, security, payments, digital enterprise (software), automation, robotics and industrial automation. Layer in advances in connectivity technologies such as 5G and you have the potential for an explosion of innovation which will not only drive significant productivity benefits but also transform the way business operates across almost every industry.

One exciting example is healthcare where the combination of genomic advances, new wearables/sensors and AI are likely to unleash new drug discovery, deeper understanding of diseases and unlock the full potential of personalised medicine. So far, recognising the enormous potential of AI, regulators have been very supportive with the FDA fast tracking approvals of AI-driven clinical imaging and diagnostics tools.

In our view, every investor and CEO, across every sector (not just the obvious ones like automotive) now needs to understand how cloud computing, AI and new connectivity technologies such as 5G will combine to reshape their industries and businesses over the next decade. Very few industries will escape unscathed but the rewards to those who understand, adapt and embrace the potential of these technologies are likely to be very significant.

Nick Evans, Ben Rogoff and Xuesong Zhao

November 2019

Important information

The information provided is not a financial promotion and does not constitute an offer or solicitation of an offer to make an investment into any fund or company managed by Polar Capital. It is not designed to contain information material to an investor’s decision to invest in Polar Capital Technology Trust plc, an Alternative Investment Fund under the Alternative Investment Fund Managers Directive 2011/61/EU (“AIFMD”) managed by Polar Capital LLP the appointed Alternative Investment Manager. Polar Capital is not rendering legal or accounting advice through this material; viewers should contact their legal and accounting professionals for such information. All opinions and estimates in this report constitute the best judgement of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document.

Polar Capital LLP is a limited liability partnership number OC314700. It is authorised and regulated by the UK Financial Conduct Authority (“FCA”) and is registered as an investment advisor with the US Securities & Exchange Commission (“SEC”). A list of members is open to inspection at the registered office, 16 Palace Street, London, SW1E 5JD.

06.12.2019

Swiss Fund & Finance Platform