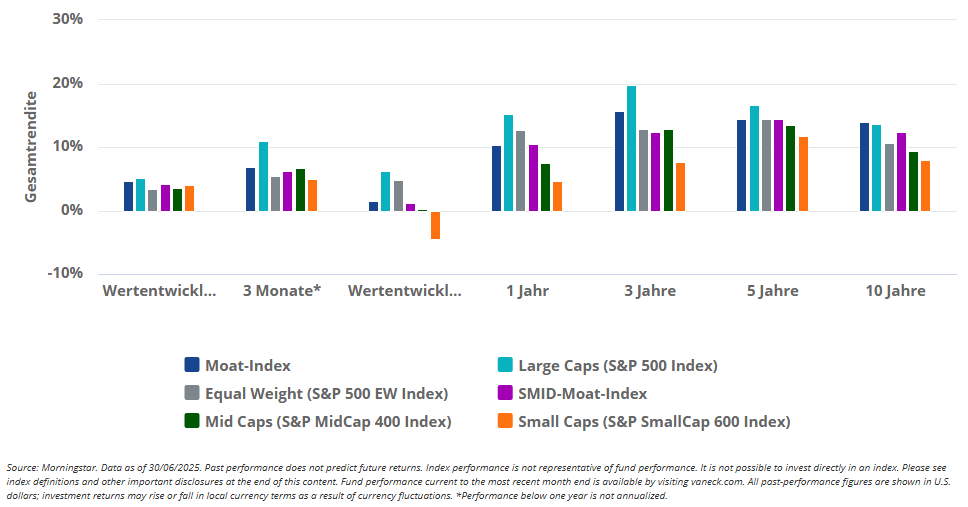

In June, U.S. equity markets sustained their May momentum, delivering an impressive summer rally as the S&P 500 and Nasdaq Composite soared to record highs. For the avoidance of doubt, all quoted numbers in this article were sourced from Morningstar. A ceasefire between Israel and Iran alleviated geopolitical tensions, while progress in U.S.-China trade negotiations eased tariff fears, boosting investor confidence. Strong corporate earnings and robust employment data further propelled optimism, pushing the S&P 500 above 6,000 for the first time since February. Technology stocks spearheaded the gains again this month, despite the Federal Reserve maintaining elevated interest rates, as investors found some assurance in updated policy rate projections that left the door open for rate cuts to begin in the second half of the year. It is worth noting that the situation on the markets was particularly turbulent this year and the drivers of performance might not persist in the future months or even change their direction entirely.

The Morningstar Wide Moat Focus Index (the “Moat Index”) participated in the June rally along with the broader equity market, posting a gain for the month. The strategy benefited from strong stock selection, allowing it to outperform the equal-weight S&P 500, and keep pace with the traditional market-weight benchmark, while also providing differentiated exposure amid a market environment that continues to be dominated by mega-cap technology. As technology stocks represent a lower weight in the Moat index, this might be a headwind when technology stocks are on the rise and lead to underperformance.

Smaller U.S. stocks, also advanced during the month, but to a lesser extent relative to large-caps, as the cohort remains laggards on the year, pressured by the persistent elevated interest rate backdrop. The Morningstar US Small-Mid Cap Moat Focus Index (the “SMID Moat Index”) posted a gain in June, outpacing both the broad small- and mid-cap benchmarks. Smaller stocks, like in the SMID moat index, may be more risky overall and might react more strongly to the potential negative sentiment in the future.

Moat Index Sees Tech Uptick at Quarterly Review

Both the Moat and SMID Moat Indexes underwent quarterly reviews on June 20, 2025. Each quarter, they systematically target the potentially most attractively priced, high-quality U.S. companies according to the Morningstar research within their respective universes. At the June review, the Moat strategies targeted valuation opportunities within technology, consumer goods and industrials. See our blog covering the recent review for more on these trends and other key insights. Full results of the quarterly reviews are also available here: Moat Index and SMID Moat Index.

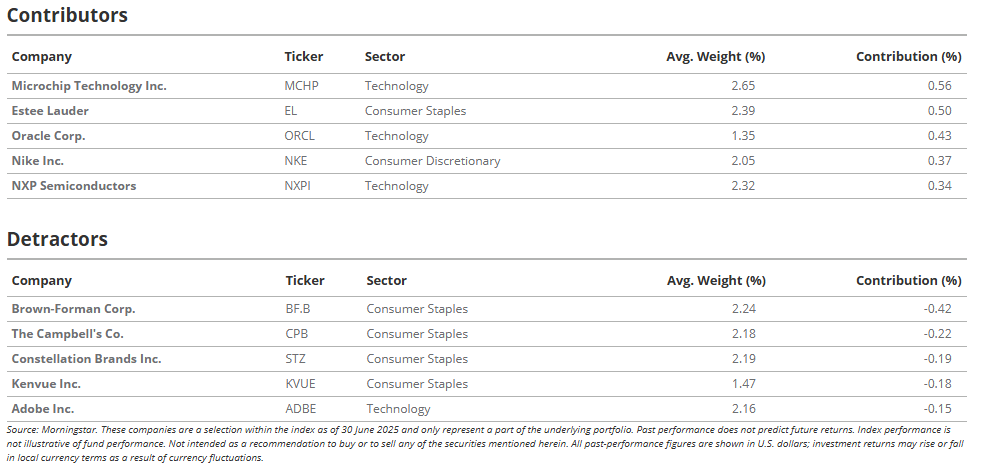

Moat Index June Highlights: Tailwinds from Tech Selection

In June, the Moat Index benefited from strong stock selection, which largely offset headwinds caused by its equal-weighted approach and current overweight positioning in defensive sectors. This enabled the Index to keep pace with the broader, tech-heavy market. Stock selection was particularly effective within the Technology sector, despite an underweight position, as highlighted by the presence of three technology names among the top five contributors. Investors should look at the longer performance periods before investing and not rely solely on the last month's returns.

The largest contributor, for the second consecutive month, was wide-moat semiconductor company Microchip Technology (MCHP). Microchip shares soared in May following strong earnings and that momentum continued in June as shares gained on analyst upgrades and market optimism. The two-month rally moved MCHP shares from $45 at the beginning of May to over $70 per share by end of June, exceeding Morningstar’s fair value estimate of $63 and leading to a trimming of the position at the recent June reconstitution in favor of other more attractive valuation opportunities. This might, of course, reverse in the future as past performance is not a guarantee of future results.

Estée Lauder (EL), a leader in premium beauty products, was also among the top contributors in June. Shares had previously faced pressure due to uncertainty around tariffs, reflecting the company’s significant global exposure, particularly in China. However, investor sentiment improved notably in June amid encouraging progress in U.S. trade negotiations, easing concerns around international market disruptions. Morningstar believes Estée Lauder remains well-positioned to benefit from consumer premiumization trends and their strategic investments aimed at expanding its presence across key emerging markets. Morningstar believes EL remains undervalued and could continue its rebound given its fair value estimate of $120 per share. While this might be the case, it is also possible that the current momentum will not continue in the future.

Other top contributors within the Moat Index during the month include the cloud enterprise application and infrastructure company, Oracle Corp. (ORCL), global footwear and apparel brand, Nike Inc. (NKE), and automotive semiconductor supplier, NXP Semiconductors (NXPI).

Companies detracting the most in June are notably from the Consumer Staples sector with four names from the segment making the list including the premium distilled spirits manufacturer, Brown-Forman (BF.B), packaged-food giant, Campbell’s (CPB), the spirits and Mexican beer importer, Constellation Brands (STZ), and consumer health company, Kenvue Inc. (KVUE). Outside of Consumer Staples is the document management and digital marketing software firm, Adobe Inc. (ADBE).

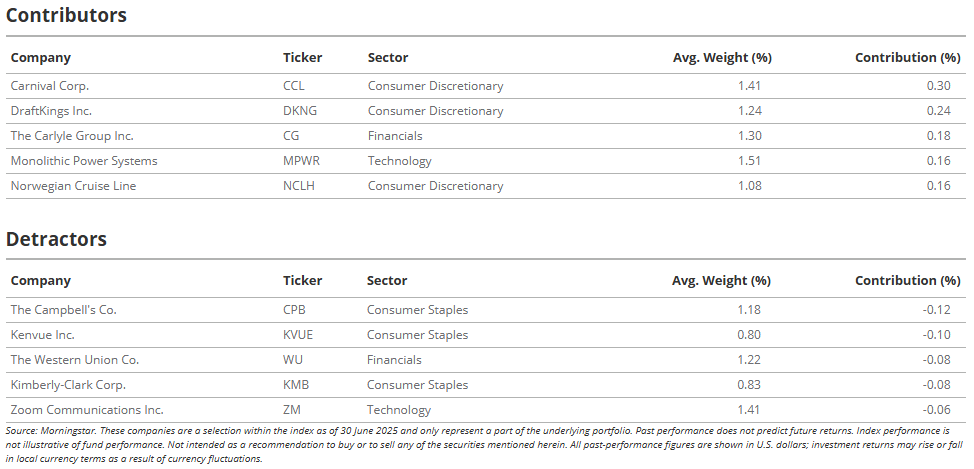

Moat Index Top Contributors and Detractors - June 2025

SMID Moat Index June Highlights: Cruise Line Momentum Continues

The SMID Moat Index outperformed both the small-cap and mid-cap benchmarks in June, supported by strong stock selection across key areas of the portfolio. Standout performance within the Consumer Discretionary and Health Care sectors led the way, helping to offset a more neutral contribution from sector positioning overall. Despite this June rally, SMID Moat stocks still underperformed large-cap stocks in June. Investors should look at the longer performance periods before investing and not rely solely on the last month's returns.

For the second straight month, Carnival Corp. (CCL) topped the SMID Moat Index, with shares rising in June. The cruise operator extended its rally after posting another quarter of impressive results, surpassing yield and cost expectations thanks to strong onboard spending and resilient late-booking demand. Management raised its 2025 net yield growth target and highlighted a booking curve that now stretches further out than ever before. With record customer deposits, a string of successful refinancing efforts, and credit-rating upgrades from S&P and Fitch, investor optimism remained strong. Morningstar lifted its fair value estimate per share for Carnival to $33 from $31 to reflect the cruise operator’s improved fundamentals and pricing strength. While this might be the case, it is also possible that the current momentum will not continue in the future.

Also powering Index performance was Norwegian Cruise Line Holdings (NCLH), which saw shares climb in June as the cruise rebound broadened. Norwegian continues to benefit from firm pricing trends and steady demand across its brands, supported by attractive itineraries, bundled offerings like the More at Sea program, and data-driven marketing. With ships sailing at full occupancy and returns on invested capital expected to reach meaningful levels in 2025, Morningstar sees the company on solid footing. Even after the strong month, Morningstar believes Norwegian shares have further upside based on their $31 fair value estimate. At the same time, the tourism sector might react particularly strongly to changes in the sentiment on the economy, and the recent returns could be eroded.

Companies detracting the most in June within the SMID Moat Index also showed a clear tilt toward the Consumer Staples sector, echoing the trend seen earlier in the Moat Index. Three of the five laggards came from the segment, including packaged-food maker Campbell’s (CPB), consumer health firm Kenvue (KVUE), and household goods manufacturer Kimberly-Clark (KMB). Rounding out the list were money-transfer provider Western Union (WU) and video conferencing software company Zoom Communications (ZM).

SMID Moat Index Top Contributors and Detractors - June 2025