Low returns have removed any incentive to save and investors, pension funds in particular, are left with an awkward dilemma of where to invest given the obvious problems with the bond market. This is effectively a magnified version of what was happening in the run-up to the financial crisis when disastrous capital allocations were made in a desperate attempt to find some yield.

Against this backdrop, emerging market (EM) hard currency debt has found some favour while local currency debt and equities have been shunned as the currency risk is viewed as being too severe. This view has been reinforced by the recent collapse in the Argentinian peso which illustrated the increasing concern that politics has become more of a threat than economics. The economics of EMs is, unusually, not a cause of great concern. Undoubtedly growth is a problem, as it is globally, and economies are performing well below potential, notably those of India, Brazil, Russia and South Africa to name a few. However, the issues that are normally a source of great concern – current account deficits, budget deficits, real effective exchange rates and inflation – are all benign suggesting risks are lower than normal. This is reflected in both bond and CDS spreads which are historically low.

Although there are, of course, exceptions banks within emerging markets are able to earn a good net interest margin without unduly punishing savers. They tend to enjoy low cost-to-income ratios and have books that are well provisioned. As a result, returns on assets tend to be much higher than in developed countries and thus returns on equity substantially above the cost of equity can be earned without excessive leverage. A strong banking system, healthy domestic finances and a low dependence on external capital leave emerging markets in a much better position to navigate a global economic downturn than has been the case historically.

EMs also offer yield. Spreads on hard currency debt have shrunk but domestic debt offers substantial real yields, albeit with a currency risk that we argue is diminished relative to the recent downturn. Dividend yields in EMs are at historically high levels relative to developed markets and yet payout ratios are substantially lower. EMs are continuing to invest to grow in countries where there is growth and not indulging in buy-backs for the benefit of option holders. Despite this, sentiment towards the asset class is at rock bottom levels, with net redemptions from equities for the past 19 weeks.

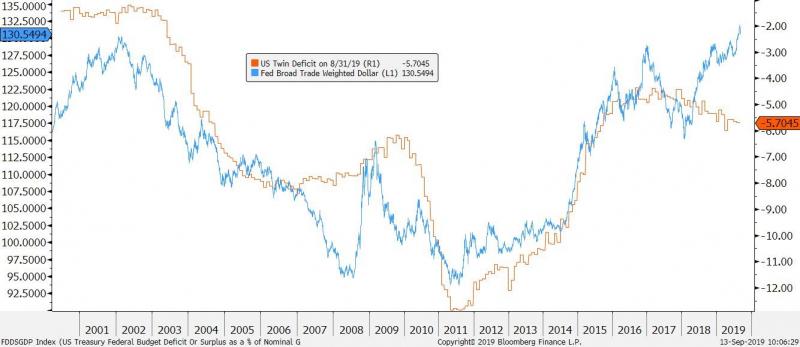

The soaring dollar is pressuring EMs as it always does, yet the fundamentals of the dollar are poor given its overvaluation on a real, effective basis allied to the deteriorating current account and budget deficits. When the dollar and the economic cycle turn, the returns in EMs can be extraordinary, as was seen in 2009. Valuations, especially in cyclicals, are getting close to the levels seen in 2008 suggesting the downside is limited – best to position ahead of the turnaround.

William Calvert, Fund Manager

Polar Capital Emerging Market Income Fund

September 2019

25.09.2019

Swiss Fund & Finance Platform

EM in a ZIRP world

Disclaimer

The information provided is not a financial promotion and does not constitute an offer or solicitation of an offer to make an investment into any fund or company managed by Polar Capital. Polar Capital is not rendering legal or accounting advice through this material; viewers should contact their legal and accounting professionals for such information. All opinions and estimates in this report constitute the best judgement of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. Past performance is not a guide to or indicative of future results.

Polar Capital LLP is a limited liability partnership number OC314700. It is authorised and regulated by the UK Financial Conduct Authority (“FCA”) and is registered as an investment advisor with the US Securities & Exchange Commission (“SEC”). A list of members is open to inspection at the registered office, 16 Palace Street, London, SW1E 5JD.