It is often easier to conceptualise ESG considerations when making investments at a corporate level. A company’s activities are often relatively narrow in focus, and forming a direct link between the company and those activities that we don’t support (polluting, gambling, smoking, drinking and so on) or those that we do (health, education, renewable resources) is usually relatively clear.

Investing in government bonds, on the other hand, raises issues that can be quite complex. When Goldman Sachs purchased Venezuelan government bonds in 2017 they were condemned for propping up an unpopular regime, while in other crises investors who sold government bonds (the original ‘bond vigilantes’) were occasionally seen as punishing the local population and subverting self-determination.

However, such complexity is not a reason to shy away from government bonds as an investment. For one, it is clear that government has a huge role to play in impacting the very forces that ESG investors care about most. From an investment perspective, they are also an asset class that can play a key role in generating return and managing portfolio risk, whether this be through long or short duration positions. This is especially important for multi asset funds which seek to deliver specific and consistent return and volatility properties across a range of environments.

Dealing with complexity. Where can we make a difference?

The wide range of activities that governments perform will mean that no government will be beyond reproach from the strictest of ESG perspectives. Defence spending is an obvious example, as are nations which have a significant reliance on fossil fuel production.

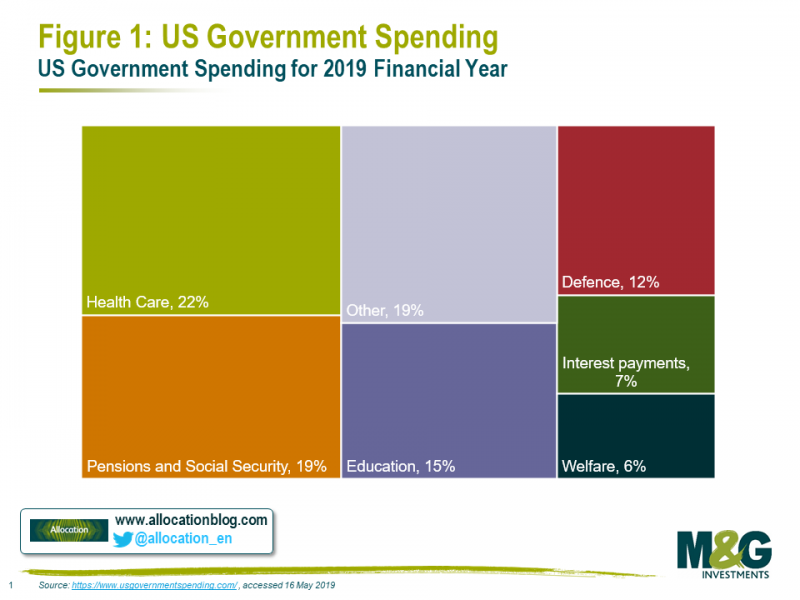

At the same time, much government spending will be made with a view to improve living standards. If we take the US as an example, although it has the largest known defence spending among nations, most of its expenditure (based on current guesstimates) is still on social care. David McCandless’ work on data visualisation provides more on putting this information into context

When viewed through this lens, it seems inappropriate to exclude US Treasury holdings simply because a government performs some activity which may not tally with ESG objectives, in the same way as we might with a single company.

Rather, we must consider whether net effects of government expenditure are beneficial. This can be challenging, but this should not be an excuse for hiding from the issue.

Political agnosticism

As the Venezuelan example illustrates, there is a risk that investing in governments can be perceived as an endorsement of a political viewpoint or support for an incumbent regime. Our view is that we should never seek to do this. In the first place our view is that we should always seek to be respectful of different views, and humble about our ability to ‘know the answer’ on how societies should be run.

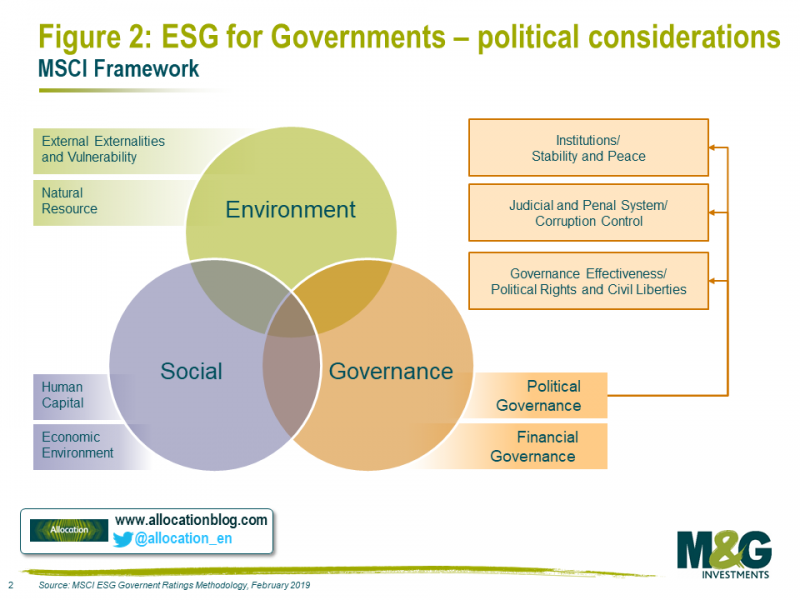

As the chart below (which is based on the methodology of MSCI’s ESG government ratings) demonstrates, assessment of institutions with regards to levels of corruption, the rule of law, and human rights are an important part of the ‘G in ESG.’.

However, just as the investment decision must be free from bias, so should these governance assessments be as free as possible for political beliefs. As we have written before, it seems that polarised political views can be a source of bias in investment decision making just as they can in any other area. Emotional reactions to particular issues or individualsare unhelpful, and taking a political stance on investment can be harmful to returns. Although the distinction can be blurry, we must seek to avoid allowing political views to colour assessments of governance and institutional structures.

Case studies

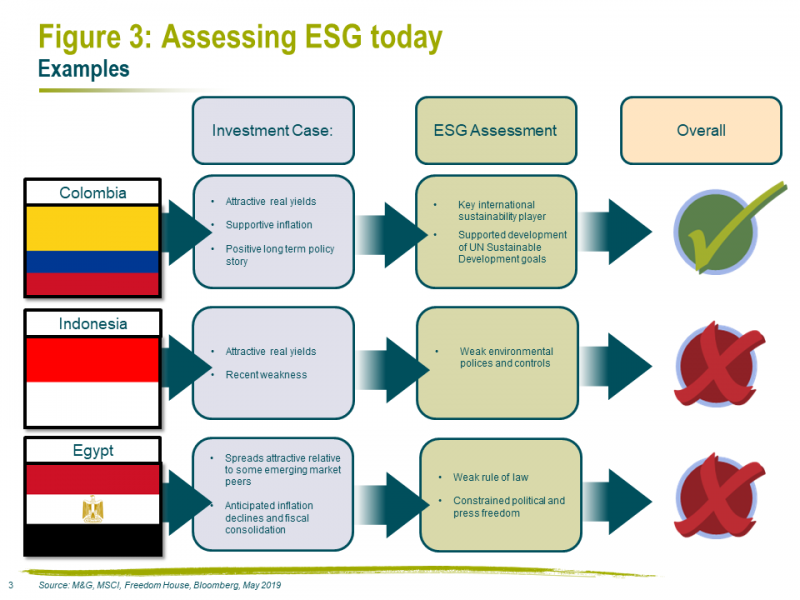

How might we apply some of these considerations? The current environment provides some useful examples. In particular, three emerging markets could be argued to be quite appealing from an investment standpoint, but when ESG considerations are taken into account two of those become far less so. Forming such judgements can be challenging in such markets where less data is available and transparency in general is poor.

.

Colombia has been one of the key sustainability players in the international arena and supported the development of the UN Sustainable Development Goals. By contrast, despite Indonesia having been given an overall ESG rating of BB by MSCI and attractive fundamentals, the country appears to lack both sufficiently strong environmental policies regarding palm oil and other environmental controls at both national and international levels. Egypt on the other hand faces challenges from a social governance perspective: irrespective of any views on the incumbent regime, prevailing institutional structures are such that organisations such as Freedom House (an independent organisation that measures and reviews indicators of freedom around the world) judge the nation to be one of the least free in the world.

Each government will entail its own variety of forces that must be considered in addition to such traditional forces as inflation, policy, and currency influences.

Conclusion

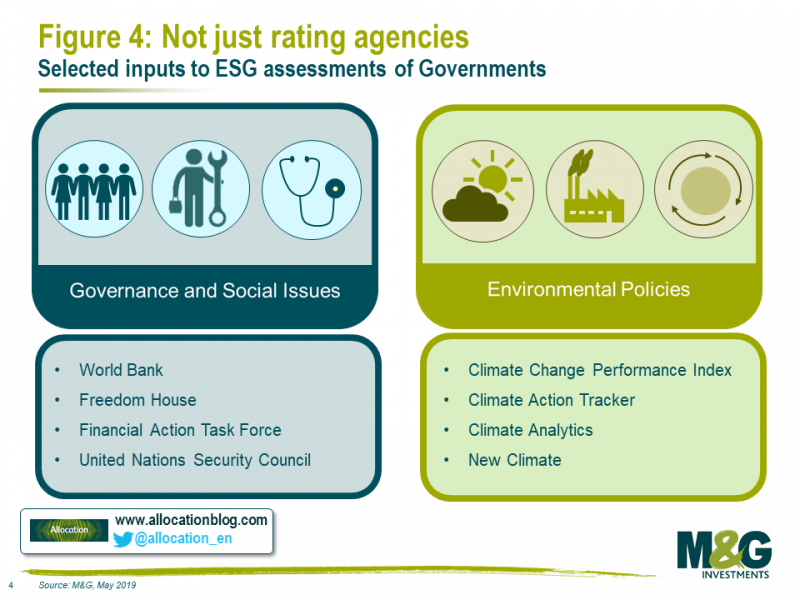

Figure 2 illustrates the range of considerations that must be taken into account when assessing government bonds from an ESG perspective. Ratings agencies like MSCI (which provide specific ESG ratings distinct from traditional credit ratings) can provide help in assessing these factors. However these must be supplemented with qualitative considerations, and other inputs such as the below:

:

Critically, there will also be significant overlap between ESG and investment considerations. Many forces related to governance will have an influence on the ability and willingness of sovereigns to pay back their debt, or levels of inflation that are expected in an economy. Living standards, health care, and education will have huge impacts on the level of productivity, and hence growth, in an economy over the long-term.

It might be easy to dismiss environmental concerns as too far off, but with climate change and extreme weather having the potential to have very real impacts on growth, and with countries such as Mexico having issued bonds with 100 year maturities in the recent past, such a view is becoming far less prevalent.

Ultimately, while assessing government bonds from an ESG perspective may be more difficult than for corporates, the role that they play is ultimately too important to ignore: both in terms of investment opportunities and – critically – in shaping the future of the world.

Maria Municchi, Fund Manager Multi-Asset at M&G Investments

06/18/2019

Swiss Fund & Finance Platform