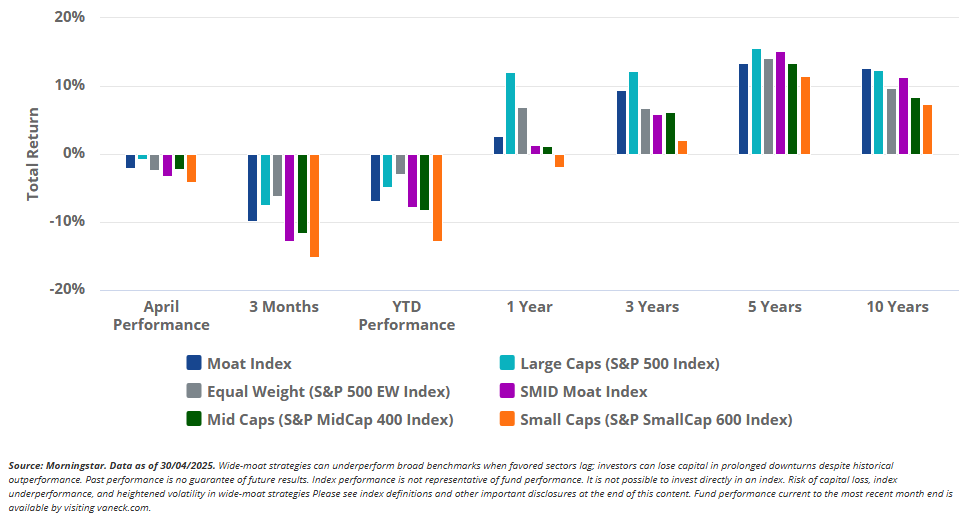

In April, volatility in U.S. equity markets intensified, as the cautious investor sentiment and trade war fears that gripped March surged to new heights following President Trump's "Liberation Day" on 2 April, which unleashed sweeping tariffs and triggered sharp retaliatory measures, sending shockwaves through global markets and deepening economic uncertainty. Equities reacted violently to the disruption, with the S&P 500 plummeting more than 10% in the days following the tariff announcement1, marking its worst week since the 2020 Covid crash. Pressures eventually eased after Trump announced a 90-day tariff pause on most nations, except China2, providing relief to a market under severe strain. However, even with a notable rebound off intra-month lows, U.S. equities finished lower in April as investors continued to digest volatile trade tensions, renewed inflation uncertainty, and the increased threat of a potential recession.

The Morningstar Wide Moat Focus Index (the "Moat Index") slipped in April, trailing the cap-weighted S&P 500's decline yet edging ahead of the S&P 500 Equal-Weighted Index's loss. Equity investments in wide-moat strategies remain subject to overall market risk and may underperform during periods when their distinctive characteristics, such as equal weighting or sector tilts, act as headwinds. The Moat Index's equally weighted construction, which spreads exposure more evenly and therefore reduces concentration in the market's largest mega-cap names, proved a headwind this month. An overweight health care position, once a tailwind earlier in the year, also worked against the Index as fresh tariff threats on pharmaceutical imports pressured the sector. Together, these factors left the Moat Index behind the broad market for the month despite beneficial exposure from other market segments.

Down market-cap, the Morningstar US Small-Mid Cap Moat Focus Index (the "SMID Moat Index") also retreated during the month, falling between the small-cap benchmark's drop and the mid-cap benchmark's more modest decline, mirroring its blended size exposure. Small- and mid-cap securities typically experience larger price swings and lower liquidity than large-cap securities, amplifying potential losses during adverse market conditions. Smaller companies were hit harder as tariff threats heightened concerns that trade tensions could drag on domestic GDP growth, a dynamic to which they are naturally more sensitive than larger multinationals. Even with the setback, the SMID Moat Index still leads both the small- and mid-cap benchmarks on a year-to-date basis3.

Moat Index April Highlights: Ships and Chips Sail Ahead

Sector positioning played a primary role in the Moat Index's relative showing against the S&P 500 in April. A complete absence of energy stocks, a group that suffered the month's steepest losses, added a tailwind, and a larger-than-benchmark stake in consumer staples and industrial names also helped. These benefits were, unfortunately, more than offset, however, by the Index's heavier weight in health care, where threats of targeted tariffs, specifically toward pharmaceutical imports, dragged the sector. Investors should remember that an overweight position in specific sectors, such as health-care and defense, increases exposure to regulatory, geopolitical and tariff-related risks that can materially lower returns.

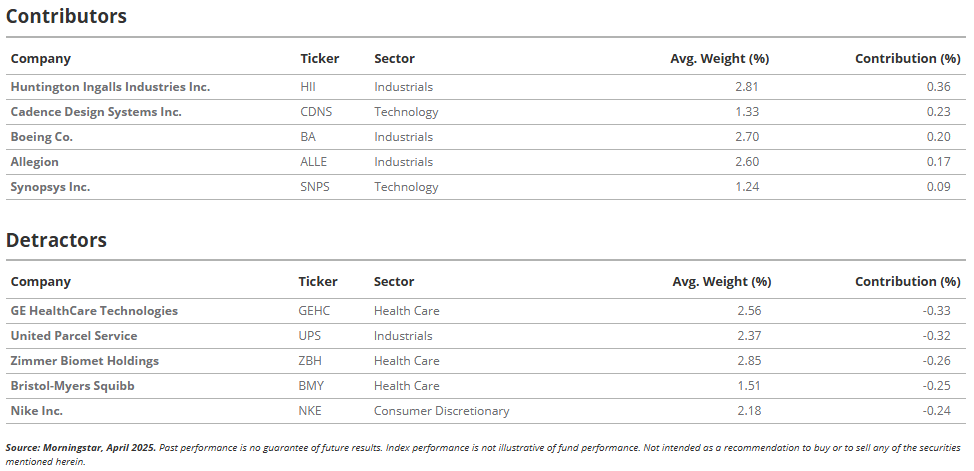

For the second straight month, wide-moat military shipbuilder Huntington Ingalls Industries (HII) held the performance crown. After sidestepping March's market turbulence, the shock steamed ahead in April on the strength of a solid first-quarter earnings beat. Momentum built further when management announced a new U.S. Navy contract for two Virginia-class submarines, coupled with fresh congressional funding to boost shipbuilding productivity4. That powerful combination catapulted HII shares into double-digit gains5 and prompted Morningstar analyst Nicolas Owens to raise his fair-value estimate to $316 on May 1st and reiterate his view that Huntington remains undervalued. It is worth noting that shipbuilding equities can also experience sharp price reversals because of defense-budget dependency and contract timing risk.

Also within the top contributors list for April is the newcomer semiconductor company Cadence Design Systems (CDNS), which just recently made its debut in the Moat Index at the March reconstitution. Cadence provides leading-edge electronic design automation tools and IP critical to the semiconductor chip design process. It benefits from switching costs and intangible assets and was upgraded to a wide moat rating from narrow in December 2024. It historically traded well above fair value until just earlier this year, allowing it to make the cut for the Moat Index. Shares of Cadence rallied 17 percent in April following positive earnings results and a steady growth trajectory amid macroeconomic uncertainty6. Despite that, semiconductor-design exposures carry elevated cyclicality and valuation-compression risk, which can quickly erode recent gains.

Other top contributors within the Moat Index during the month include the well-known aerospace and defense giant Boeing Co. (BA), global security products and solutions company Allegion (ALLE), and the semiconductor design software provider Synopsys (SNPS).

Detracting most this month were companies particularly impacted by tariff uncertainty, several belonging to the health care sector, including leading medical technology firm GE HealthCare Technologies (GEHC), orthopedic implants provider Zimmer Biomet (ZBH), and drug manufacturer Bristol Myers Squibb (BMY). Footwear and apparel brand Nike (NKE) and the world's largest parcel delivery company, United Parcel Service (UPS), both heavily influenced by tariffs, were also notable detractors.

Moat Index Top Contributors and Detractors - April 2025

SMID Moat Index April Highlights: Data Centers Keep Their Cool

The SMID Moat Index's April performance benefited from favorable sector positioningrelative to the mid-cap benchmark, with underweights in financials and real estate, two of the weaker-performing sectors, alongside a higher allocation to technology stocks, which provided a modest lift. However, those advantages were offset by stock-specific weakness, stemming from names that were disproportionately affected by the heightened tariff uncertainty.

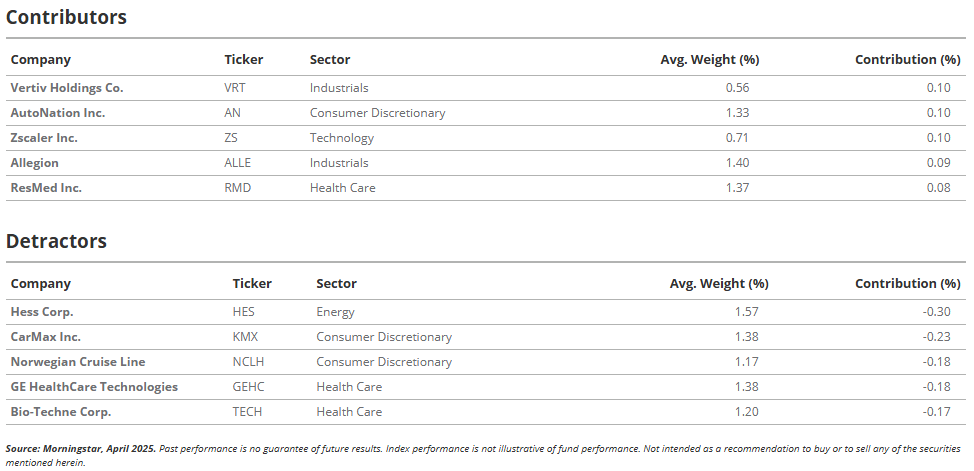

Vertiv Holdings Co. (VRT) defied April's market volatility, gaining 18 percent7 only weeks after joining the SMID Moat Index in the March reconstitution. Investors shall remember that rapid price appreciation in individual holdings can reverse quickly; concentrated exposure to technology infrastructure increases downside risk in cyclical slowdowns. The surge followed a standout first-quarter report that delivered 25 percent year-over-year organic revenue growth and nearly 50 percent earnings-per share expansion. Management also lifted full-year sales guidance by approximately three percentage points. The robust results reinforced investor confidence in Vertiv's key role in supplying critical infrastructure equipment, primarily power management and cooling systems, to data centers increasingly focused on cloud computing and AI-driven workloads.

Morningstar assigns Vertiv a narrow economic moat, reflecting the durability of its Liebert brand, which maintains leading market positions in thermal management and power equipment, as well as customer relationships that frequently span more than two decades. Analyst Nicholas Lieb, CFA, maintains a $103 fair-value estimate, citing Vertiv's pricing power and the essential nature of its products as valuable safeguards against potential tariff-related cost pressures arising from its manufacturing facilities in Mexico and component sourcing from China.

Other notable gainers in April included the automobile retailer AutoNation (AN), cloud-native cybersecurity software provider Zscaler (ZS), global security products and solutions company Allegion (ALLE), as well as respiratory care and medical device developer ResMed (RMD).

The biggest laggards were independent oil and gas producer Hess Corp. (HES), the largest domestic used-vehicle retailer CarMax (KMX), cruise line operator and travel service provider Norwegian Cruise Line (NCLH), medical technology firm GE HealthCare Technologies (GEHC), and protein sciences market leader Bio-Techne Corp. (TECH).

SMID Moat Index Top Contributors and Detractors - April 2025

1 Bloomberg, 03-05 Apr 2025 intraday data.

2 CNBC, 9 April 2025, https://www.cnbc.com/2025/04/09/trump-announces-90-day-tariff-pause-for-at-least-some-countries.html

3 Morningstar, 30 Apr 2025.

4 U.S. Navy, 30 April 2025, https://www.navy.mil/Press-Office/News-Stories/display-news/Article/4170873/navy-awards-contract-modification-for-two-additional-virginia-class-submarines/

5 Morningstar, 01-31 March 2025, 01-30 April 2025.

6 Morningstar, 01-30 April 2025.

7 Morningstar, 01-30 April 2025