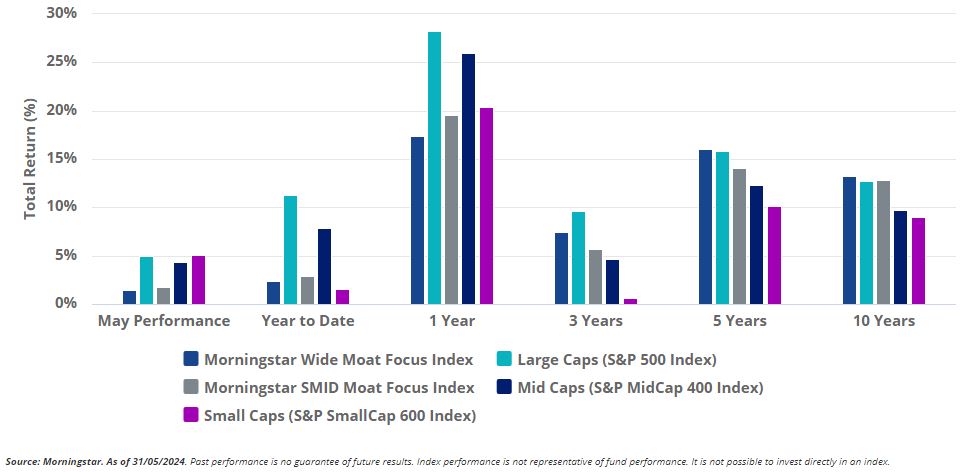

US equities re-initiated their upward trend in May with markets ending the month higher, but not without some volatility. To start the month, the three major US stock indices rallied from prior month declines and not only fully recovered from April drawdowns but went on to set new all-time highs by mid-May. Helping move markets higher was positive inflation data and quarterly earnings results. However, ending the month was a divergence in performance between AI-tangential tech and nearly everything else. The Dow Jones Industrial Average slid over 4% from its new high water mark, giving up much of its gains to end the month up slightly, while the S&P 500 and Nasdaq finished May up a noteworthy 5% and 7%, respectively. Once again it was the narrow leadership of mega-cap tech supporting the market with Nvidia, Apple, Alphabet, Microsoft and Meta accounting for 60% of the S&P 500’s return in May. Notably though, signs of doubt appeared in big tech on the final trading day of the month with the Nasdaq falling nearly 2% intraday before mounting a late day rally to close flat.

The Morningstar Wide Moat Focus Index (the “Moat Index”) May performance was disappointing, lagging the S&P 500 by more than 300 basis points. The Moat Index suffered from its equal-weighting scheme, bias toward value, and simply not owning Nvidia and other mega-cap technology names. These are the same headwinds that have challenged the Index for much of the year, leading to a frustrating 2024, so far, for moat investing patrons. However, with a more than 15-year track record, this is not the first period of underperformance for the Moat Index, and more importantly, these difficult periods have historically been followed by periods with some of the strongest outperformance. More on this later.

Smaller US companies also rebounded in May, following steep April declines, with the small- and mid-cap broad benchmarks keeping pace with the S&P 500 during the month. The rally moved small-caps back into positive territory for the year while mid-caps held their notable lead but still lagged large-caps. The Morningstar US Small-Mid Cap Moat Focus Index (the “SMID Moat Index”), however did not fully participate in the rally suffering from poor stock selection, despite positive sector positioning.

Moat Stocks Faced Strong Headwinds in May | As of 31/05/2024

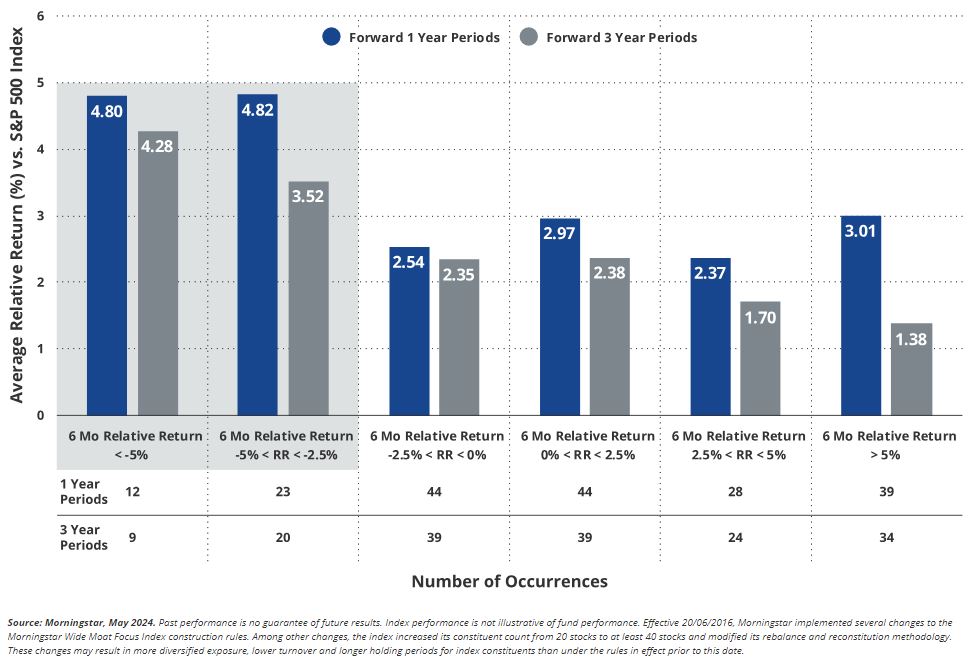

History Suggests Better Days Ahead for Moat Stocks

The Moat Index has faced challenging headwinds for much of this year given its equal-weighting approach amidst a market with narrow leadership and record levels of concentration. While it can be tough to weather periods of underperformance, subscribers of the Moat Investing philosophy have often been rewarded on the other side of the storm. Historically, the Moat Index has had its strongest relative performance following periods of notable underperformance.

During the more than 15 years of live history for the Moat Index, when it has underperformed the S&P 500 by more than 2.5% in any six-month period, the Index has gone on to substantially outperform in the following 1- and 3-year periods. In fact, the Moat Index has outperformed the S&P 500 by an average of 4.28% annually in the 3 years following six-month periods with greater than -5% relative performance. While history is no guarantee, it can still serve as a useful guide, and the historical context suggests potentially better days ahead for moat stocks.

Outperformance Historically Followed Periods of Underperformance | 28/02/2007 - 31/05/2024

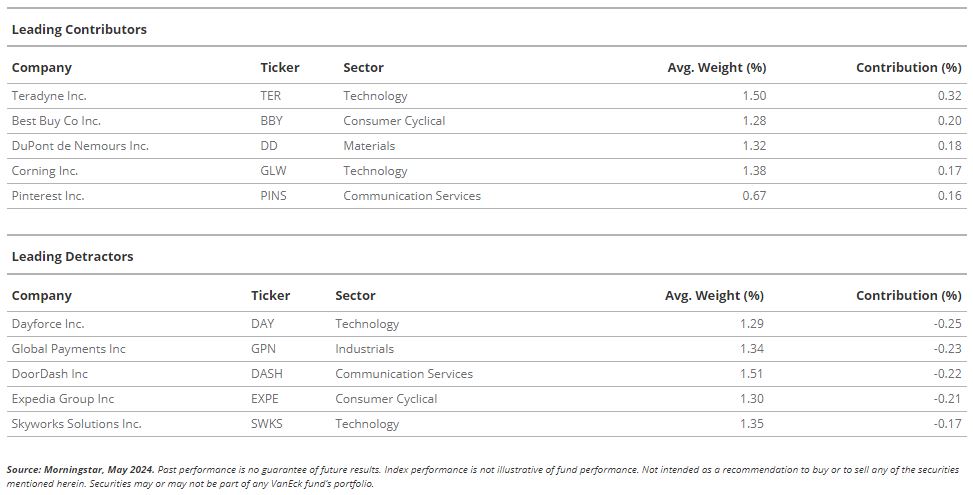

Moat Index Top Contributors and Detractors

While Nvidia does not currently make the cut for the Moat Index, that doesn’t mean the index has no exposure to the semiconductor market. The Moat Index instead includes the perhaps lesser-known semiconductor equipment and materials company Teradyne (TER) which gained over 20% in May, landing it at the top of the list in terms of contributors to performance during the month.

Teradyne is a heavyweight supplier of automated test equipment for semiconductors, boasting market-leading capabilities that run the gamut of chips. It is one of two companies worldwide that can produce testers for the most cutting-edge semiconductors, thanks to robust engineering talent across hardware and software and a structural lead in organic investment. The firm is a vital partner to chipmakers across the industry and has an impressively strong relationship with Apple and Taiwan Semiconductor. Teradyne’s market leadership exhibits itself in industry-leading margins, strong returns on invested capital, and a top market share. Following its rise in May, the stock now trades just about on par with Morningstar’s $135 estimate of fair value.

The largest detractor to performance within the Moat Index during the month was beauty products company Estee Lauder (EL). Estee Lauder fell more than 15% in May following mixed earnings results which showed beats on revenue and earnings per share, but soured investors with lower than expected guidance. Despite the negative reaction by the market, Morningstar was encouraged by Estee Lauder’s inventory management, agility in product innovation and consumer-facing initiatives which combined to fuel top-line growth and drove gross margin expansion. Morningstar also sees EL as being poised to benefit from growth opportunities in global markets like Asia, India and Brazil as middle-market consumers upgrade from lower quality mass brands. EL currently trades at a 40% discount to Morningstar’s $210 estimate of fair value.

Top Contributors and Detractors from Moat Index - May 2024

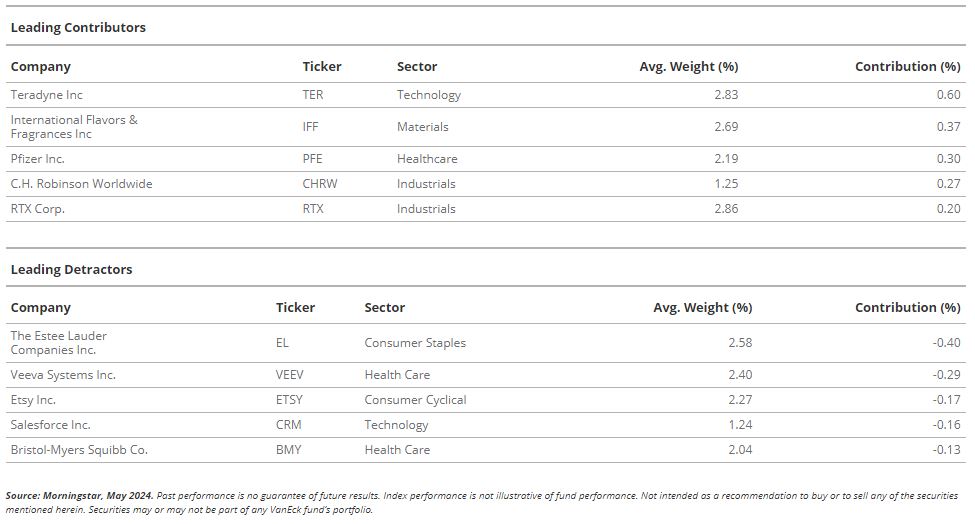

SMID Moat Index Top Contributors and Detractors

The smaller cap SMID Moat Index also benefited from the above-mentioned Teradyne (TER) as the mid-cap stock’s May performance led the pack of SMID moat companies as well. Consumer electronics retailer Best Buy (BBY) was also a top contributor for the month following a late month better than expected earnings results that sent the shares up nearly 20% in the final days of May. Morningstar noted Best Buy’s revenue and earnings results were largely in line with their expectations and that the rapid repricing of the stock was likely reflecting the market’s unnecessarily dim top-line expectations before the earnings release. Morningstar maintained their $90 estimate of fair value for Best Buy with shares of the company ending the month trading in the mid-$80 range.

Names that most negatively contributed to the SMID Moat Index performance during the month include payroll and human capital management software solutions company Dayforce (DAY), global payment processing and software solutions company Global Payments (GPN), online food order aggregator and deliverer DoorDash (DASH), and travel services agency Expedia (EXPE) which all declined double digits in May.

Top Contributors and Detractors from SMID Moat Index - May 2024